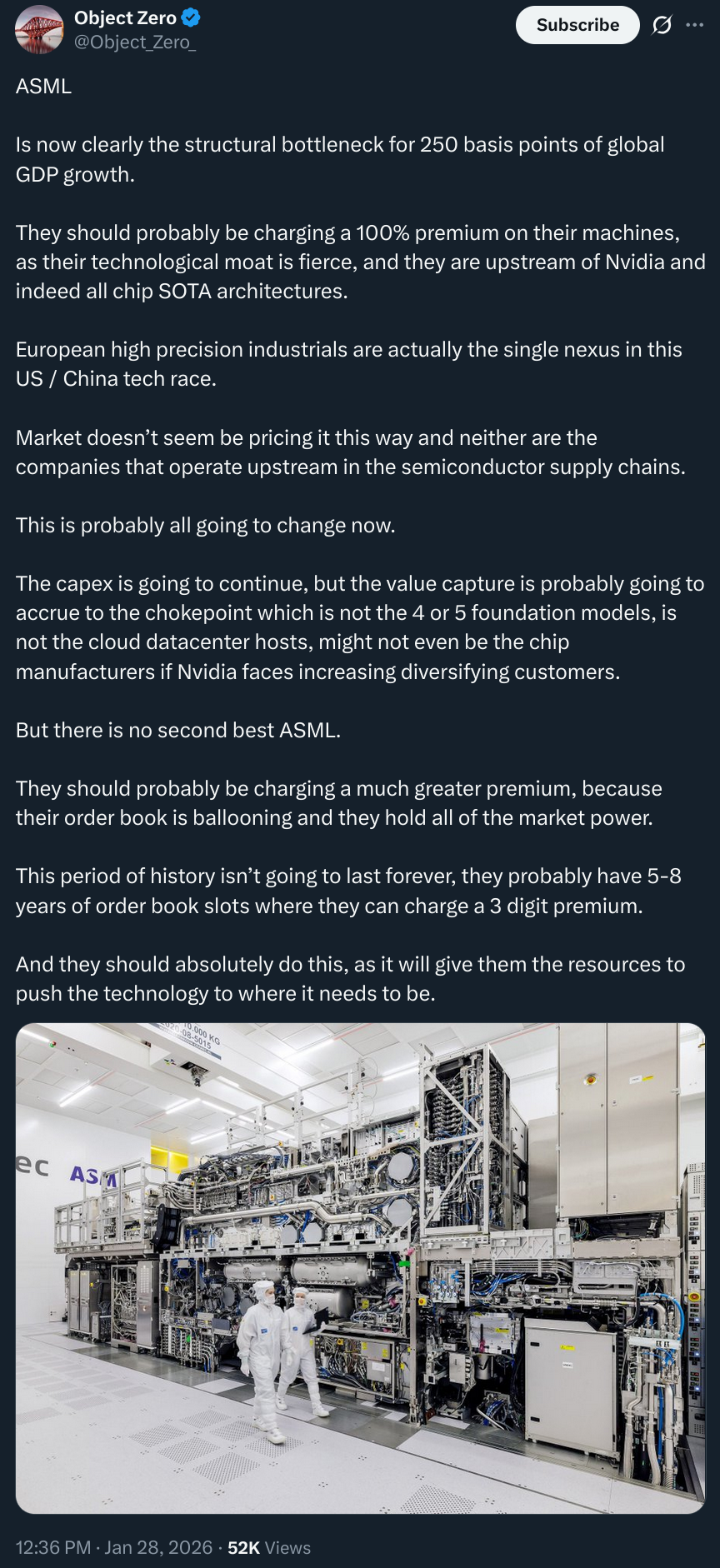

"They should probably be charging a 100% premium on their machines"

- writes the Anglo-Saxon about chip equipment manufacturer ASML

Anglo-Saxons don't get it

What we're seeing here is a deep cultural divide running right through the Western world between UK/USA and DACH/NL/Scandinavia.

The Anglo-Saxon sees: "ASML has such a massive technological lead, they could double their prices without facing immediate competition"

This exact mindset leads to many financially breathtakingly successful companies that nobody actually likes: Google, Microsoft, Oracle....

What the Anglo-Saxon overlooks

This exact mindset leads to weakness in sectors that require long-term stable commitment with permanently high research intensity.

These sectors are not randomly dominated by Central European companies.

Take the example of ASML.

It's not like they never had competition or like their place on the throne is set in stone.

In the "early days" of the semiconductor industry, Americans were actually leading (GCA, Silicon Valley Group, Perkin-Elmer etc.).

Up through DUV nodes (simplified: machines for the second-newest chip generation), Japanese firms like Canon and Nikon (yes, the camera companies) were very important competitors.

For EUV (newest generation), ASML is alone. Not because Dutch engineers are smarter than Californian or Japanese ones – but because of culturally and structurally extremely long staying power.

Partnership instead of "Value Extraction"

ASML maintains a more "partnership-based" relationship with both key customers like TSMC and suppliers like Zeiss or Trumpf, rather than optimizing for maximum short-term "value extraction," and has an interesting corporate structure:

The company is "publicly traded with a sword of Damocles"

ASML is openly traded on the stock exchange and can thus easily raise capital, but is "poisoned" for activist investors through a foundation construct.

The "Stichting Preferente Aandelen ASML" has the statutory mandate to ward off external influences on ASML, and a contractual option to buy preference shares at nominal value.

Zeiss: 180 years at the top

The supplier for the most critical core optical components like the mirrors etc. is Zeiss. A German company that turns 180 years old this year and has been permanently at the absolute forefront of optical technology since its founding.

The kicker? It has belonged entirely to a foundation since 1896, going back to the founder and his first "CTO" Ernst Abbe.

More examples in the "Long Game High Tech" space

We have more such examples in the "Long Game High Tech" space:

- Bosch (Electronics/Automotive, Germany)

- Novo Nordisk (Pharma, Denmark)

- Lundbeck (Neuroscience/Pharma, Denmark)

- Carlsberg (Brewery, Denmark)1

- Ericsson (Telecom, Sweden)

- Rolex (Luxury watches, Switzerland)

- DNV (Maritime, Norway)

- ...and plenty more.

The pattern: Foundations as "dead hand"

What all these firms have in common is that they're either outright owned by a foundation, or a foundation as the "dead hand" of the founders continues to exercise control rights into the present....

...and that they all come from a contiguous cultural space that stretches from Switzerland to Sweden, but explicitly not other Western countries like UK/USA or even France or Spain.

Carlsberg is historically very significant in the "scientification" of brewing, bottom-fermenting lager yeasts are technically termed "Saccharomyces carlsbergensis"↩